Today's release of the Household Misery Index showed that the level of misery declined in February dropping 0.04% but still remained near the peak for this cycle and nearly the highest level seen in 30 years while on a year-over-year basis, misery declined for the third consecutive month dropping 0.14% since February 2010.

Back in the 1970s and 80s the “

Misery Index” was popularized as a measure that accurately captured the misery and malaise of the time.

The original Misery Index was a bit too simplistic as it only captured the severity of the two main vexing issues of the time, unemployment and inflation.

Today, inflation, as measured by the annual rate of change of the CPI-U, is not a significant source of financial misery.

Of course, households on fixed income may dispute that fact and many have argued that CPI itself does not accurately capture “real” inflation as it has never accounted for the ridiculous increasing costs of housing and other essentials so for the sake of formulating a new misery index, inflation will factored out.

Another key to formulating a new misery index is to specifically target “household” misery as opposed to including data that might target the miserable state of affairs of the federal government or corporate misery.

The Household Misery Index captures the following trends and weights them equally:

1. The U-3 unemployment rate

2. YOY percent change of the 10-Year moving average of total nonfarm payrolls

3. YOY percent change of the 10-Year moving average of “real” personal income

4. YOY percent change of the 10-year moving average of “real” S&P 500

The unemployment rate captures the misery associated to the threat and severity of a potential bout of unemployment while the annual change of the 10 year moving average of non-farm payrolls captures a more fundamental sense of the overall job market.

The annual change to the 10 year moving average of “real” (adjusted with CPI-U) personal income captures a household’s long term sense of income prospects.

The annual change to the 10 year moving average of “real” (adjusted with CPI-U) S&P 500 captures a household’s long term sense of typical investment prospects.

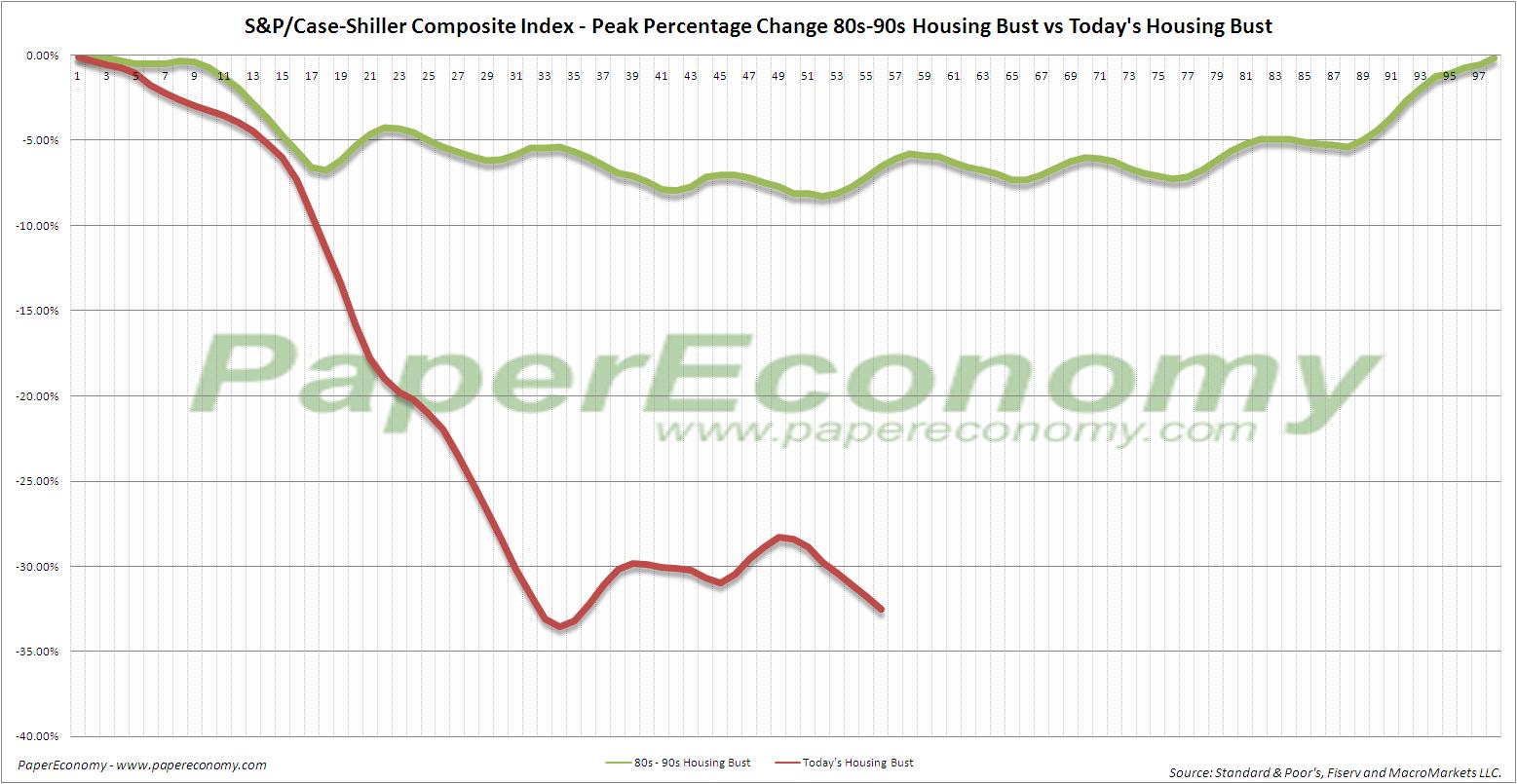

Unfortunately, all home price series are simply not long enough to include in the formulation but there may be alternative measures that can be included in the future.

This is a notable improvement for misery and if the past is to be taken to be even just a crude guide, the level of household misery should continue to steadily improve in the coming months.

The latest release of the Fannie Mae Monthly Summary indicated that for data through February, total serious single family delinquency continued to declined though at a notably slower pace than in recent months.

The latest release of the Fannie Mae Monthly Summary indicated that for data through February, total serious single family delinquency continued to declined though at a notably slower pace than in recent months.