Like this post? Consider subscribing to my Substack for additional insights and content today!

One of the major differences between our current housing boom and the epic housing run-up and associated crash that ultimately led to the “Great Recession” is in the supposed quality of buyers, or more precisely, the underwriting standards lenders use when making home loans as well as the soundness of the loan products and features they offer.

Without a doubt, lending standards by 2005/06/07 had become completely detached from reality with 100% loan-to-value, no-interest, reverse amortization, no-income verification, sub-prime being some of the various means by which the housing finance system kept the party going (loan volume) even after prices had risen well out of reach for many prospective home buyers.

In the aftermath of the epic financial meltdown that ensued, there was a notable effort by Federal regulators to understand what went wrong, and further, to take measures to prevent such egregious activities in the future.

The Dodd-Frank “Wall Street Reform and Consumer Protection” Act had as a provision the “Mortgage Reform and Anti-Predatory Lending Act” which sought in part to tighten up the process of mortgage origination in order to:

It is the purpose of this section and section 129C to assure that consumers are offered and receive residential mortgage loans on terms that reasonably reflect their ability to repay the loans and that are understandable and not unfair, deceptive or abusive.

To that end there are the following two important sub-sections (NOTE: Dodd-Frank is an enormous act with many provisions; these are just two small samples of items focused specifically on mortgage origination standards):

Subtitle B: Minimum Standards for Mortgages

IN GENERAL.—In accordance with regulations prescribed by the Board, no creditor may make a residential mortgage loan unless the creditor makes a reasonable and good faith determination based on verified and documented information that, at the time the loan is consummated, the consumer has a reasonable ability to repay the loan, according to its terms, and all applicable taxes, insurance (including mortgage guarantee insurance), and assessments.

This section goes on to detail tighter rules for regulating, multiple loans (borrowers has subordinate loans on same property), income verification, no-interest options, negative amortization options and other lending phenomena that contributed to the mortgage mania of that era.

Subtitle F: Appraisal Activities

IN GENERAL.—A creditor may not extend credit in the form of a subprime mortgage to any consumer without first obtaining a written appraisal of the property to be mortgaged prepared in accordance with the requirements of this section.

This section goes on to detail tighter rules for regulating the appraisal process of a property that will be financed using a “high-risk” subprime loan.

Taken together, these two sub-sections point to one major flaw in the legislative financial regulatory process in that it is at best always backward looking, specifically addressing practices that occurred in the past that had led to financial crisis.

Whether there is any sense to even trying to regulate future financial activities, is not the topic of this post, but suffice to say, the Dodd-Frank mortgage origination related provisions focused heavily on the activities that led to the Great Recession and didn’t attempt to regulate other novel methods that might be employed in future speculative episodes.

One area that I have taken an interest in is in the non-conforming “jumbo” loan market and particularly in my own market of Boston where throughout 2020, 2021 and on into 2022, I have witnessed some truly reckless behavior on the part of borrowers and lenders.

Following up on my prior post on the subject, I dug a little deeper into the homes that I have highlighted previously to better understand the nature of the debt that financed these reckless purchases.

From a traditional mortgage lending perspective, these purchases appear pretty sound given that the average loan-to-value (LTV) was about 70% (i.e. 70% loan, 30% deposit), all mortgages were simple 30-year fixed rate loans (no risky options or even a single ARM) and I assume that all incomes were verified.

But considering that each of these buyers over-bid the listing price by on average a whopping 30%, one might draw a different conclusion.

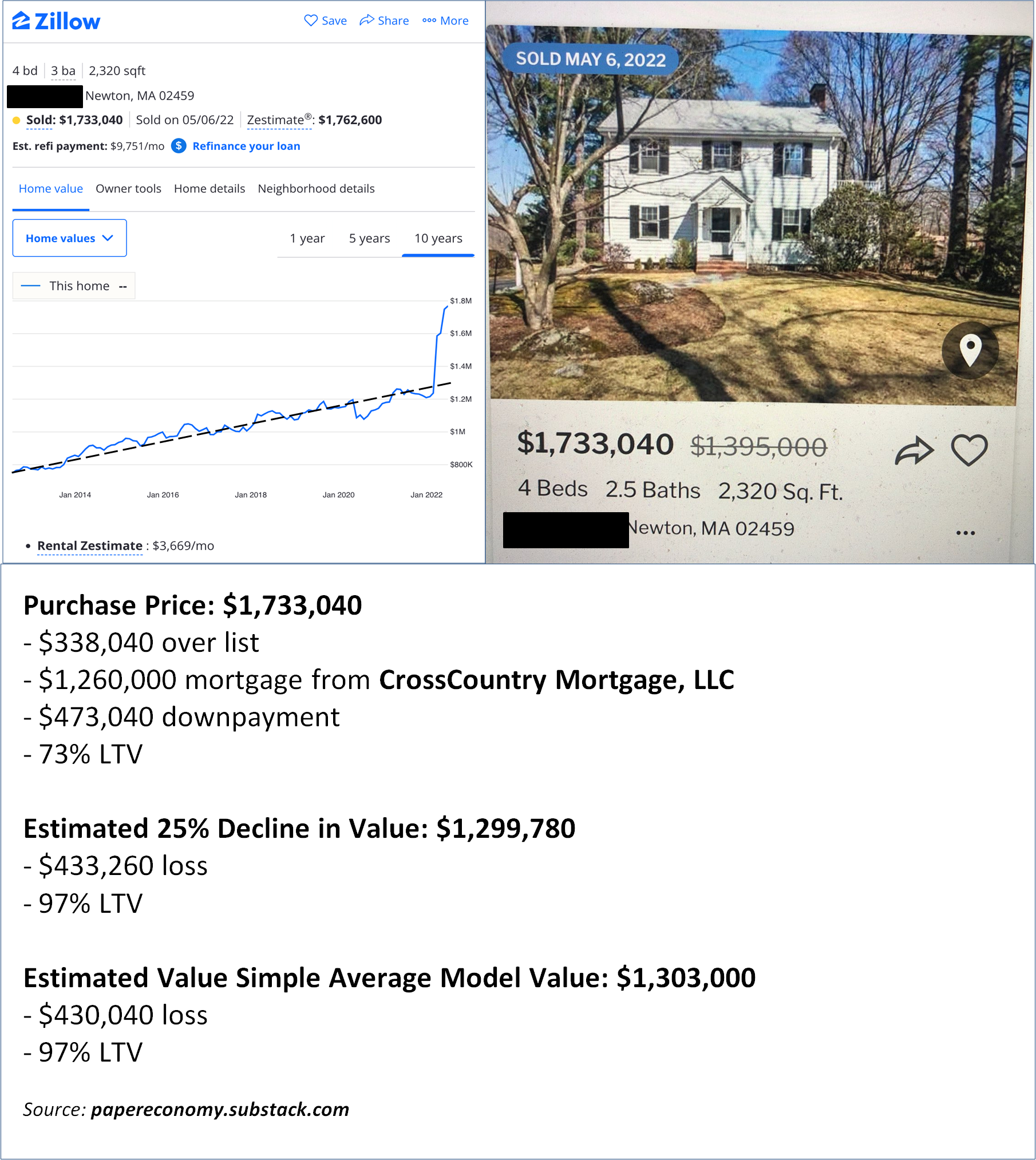

First, below is a simple average model for pricing the Boston housing market that I developed using the S&P CoreLogic Case Shiller Home Price Index (CSI) for Boston. This model, superimposed on a Zillow price history, simply uses the CSI to calculate the price trend line with 2016-2019 based on actual annual price changes and 2020-2022 based on an average annual price change from the trailing eight (8) years.

My general premise with this model is that 2020 through 2022 represented an absurdly anomalous period where lending rates were exceptionally low and buyers (as a result of COVID-19 hysteria) were simply not acting prudently.

As you can see from the model, there is a significant risk of “mean reversion” for the nation’s severely overheated housing markets as interest rates rise and prices fall meeting a more fundamental balance that, once materialized, will call into question the financial soundness of the loans backing up these properties.

If, given the emerging headwinds for the macro economy and housing specifically, we see a 25% pullback in home prices in Boston (not inconceivable given the ferocity of the price appreciation in just the last two years as well as the scale of prior pullbacks of about 16% after the late-80s S&L crisis and 18% after the Great Recession), then these homes would all have an average LTV of about 92%, a much less sound financial footing for these buyers and lenders.

Further, many of the homes could fall even more sharply given how far off the simple average price trend (the model) the buyers pushed the purchase with their manic bidding.

The following is a selection of three homes from my original post, annotated with the simple average price model as well as the mortgage details to illustrate the point:

Note that I calculated the LTV as they stood on the day of settlement as well as what the LTVs would be after both a 25% pullback in prices as well as with respect to the simple average price model forecast of the more fundamentals-based value.

The loophole in the lending standards for this cycle appears to have been that home appraisals were either unable to accurately account for the outlandish price appreciation occurring in the market or were simply roundly ignored given the fact that borrowers came to the table with 20%-30% down-payments and had good credit histories.

Prudent lenders would have evaluated the appraisal to determine a more fundamental valuation and either demanded more down-payment from the bid-happy borrowers to account for the additional risk or simply rejected the transactions outright.

For example, for the first property above, the fundamental value of the home at the time of purchase was probably closer to about $1,300,000 but it was bid up to $1,720,000 or about $420,000 over its fundamental price.

If the lender had been more prudent, they would have either walked away from the transaction or demanded that the borrower come up with about $800,000 for the deposit instead of the meager $400,000 that the borrower actually paid.

This would have resulted in a loan of about $920,000 against an $800,000 deposit for a very healthy 53% LTV which would have been well fortified against any oncoming economic crisis-driven home price decline.

Obviously, the lender didn’t perform this level of due-diligence because the borrow could not afford the additional deposit and all parties involved (lender, broker, lawyers, buyer and seller) simply wanted to stack up another closed transaction.

I suspect that my small sample is clearly demonstrating something important about the housing market dynamics this cycle, namely that there is real, yet to be fully realized, systemic risk coming from the prime lending market particularly for the performance of privately funded “jumbo” loans.